Why a Pre-Settlement Walkthrough in Florida Can Save You Thousands

Buying a home is one of the most significant financial decisions you’ll ever make. In Florida’s competitive mortgage loan market, ensuring that your investment is protected is crucial. One essential step in this process is the pre-settlement walkthrough—a final inspection of the property before closing. This walkthrough helps buyers confirm that the home is in the agreed-upon condition, ensuring there are no last-minute surprises.

What Is a Pre-Settlement Walkthrough?

A pre-settlement walkthrough is a buyer’s last opportunity to inspect the property before finalizing the purchase. It typically occurs 24 to 48 hours before closing and allows buyers to verify that:

The home is in the same condition as when they agreed to purchase it.

Any agreed-upon repairs have been completed.

Fixtures and appliances included in the sale are still present.

No new damages have occurred since the last inspection.

Why Is It Important?

Skipping a pre-settlement walkthrough can lead to unexpected issues that may be costly to fix after closing. Here are some key reasons why this step is essential:

1. Identifying Last-Minute Issues

Between signing the contract and closing, several weeks may pass. During this time, unforeseen problems can arise, such as:

Water damage from leaks or storms.

Electrical or plumbing failures due to aging systems.

Pest infestations that were not present during previous inspections.

According to a study by the National Association of Realtors (NAR), 30% of homebuyers encounter unexpected issues after moving in, many of which could have been identified during a walkthrough.

2. Ensuring Repairs Are Completed

If the seller agreed to make repairs, the walkthrough is the time to verify that they were completed properly. A report from HomeAdvisor states that the average cost of home repairs in Florida ranges from $500 to $5,000, depending on the severity of the issue. Catching incomplete repairs before closing can save buyers from unexpected expenses.

3. Confirming Inclusions

Buyers should ensure that all agreed-upon fixtures, appliances, and other items remain in the home. Common disputes include missing:

Kitchen appliances

Light fixtures

Built-in shelving

A survey by Zillow found that 22% of homebuyers reported missing items after moving in. A walkthrough helps prevent such disputes.

How to Conduct a Thorough Walkthrough

To maximize the effectiveness of your walkthrough, follow these steps:

1. Bring a Checklist

Having a checklist ensures that you don’t overlook important details. Key items to inspect include:

Walls, ceilings, and floors for damage

Plumbing (run faucets, flush toilets)

Electrical systems (test lights, outlets)

HVAC system (check heating and cooling)

Appliances (test functionality)

Doors and windows (ensure they open and close properly)

2. Document Any Issues

Take photos or videos of any concerns and notify your real estate agent immediately. If necessary, request that the seller address the problems before closing.

3. Test Everything

Turn on lights, run water, check heating and cooling systems, and ensure all appliances work. This step prevents post-move-in surprises.

What If You Find Problems?

If issues arise during the walkthrough, buyers have several options:

Request repairs before closing.

Negotiate a credit to cover repair costs.

Delay closing until the issues are resolved.

According to Florida Realtors, 15% of home sales experience delays due to last-minute issues found during walkthroughs. Addressing concerns early helps avoid complications.

Conclusion

A pre-settlement walkthrough is a crucial step in the home-buying process, ensuring that buyers receive the property in the expected condition. By taking the time to inspect the home thoroughly, buyers can avoid costly surprises and protect their investment. In Florida’s dynamic mortgage market, being proactive can make all the difference.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Lamas Loans, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Investing in Real Estate? Here’s Why Location Is the #1 Factor in 2025’s Housing Market

In the ever-evolving world of real estate, one truth remains constant: location is king. While factors like home size, amenities, and design play a role in property value, location continues to be the most influential factor in determining a property’s desirability and long-term investment potential. As we step into 2025, location matters more than ever due to shifting market dynamics, technological advancements, and changing buyer preferences. Let’s explore why location is the driving force behind real estate decisions today.

The Power of Location in Property Value

Real estate experts have long emphasized that location is the single most important factor in determining property value. In 2025, this principle holds stronger than ever. According to recent market analyses, homes in prime locations—such as urban centers, coastal regions, and areas with strong infrastructure—continue to appreciate at a faster rate than those in less desirable locations.

For instance, properties in high-demand metropolitan areas have seen an average price increase of 8-12% annually, compared to 3-5% in suburban and rural areas. This trend highlights the importance of choosing a location with strong economic growth, accessibility, and amenities.

The Rise of 15-Minute Cities

Urban planning trends like the “15-minute city” are redefining what makes a location desirable. This concept focuses on creating communities where residents can meet most of their daily needs—work, shopping, healthcare, and entertainment—within a 15-minute walk or bike ride. Cities adopting this model, such as Paris, Melbourne, and Portland, are experiencing surging interest from investors and buyers who value convenience and sustainability.

The Work-from-Home Effect

Environmental risks such as flooding, wildfires, and extreme weather are reshaping the real estate map. Buyers are increasingly factoring in climate resilience when choosing a location. Cities investing in sustainable infrastructure and disaster mitigation plans are commanding premium prices. Coastal properties remain desirable, but buyers are more cautious, favoring areas with robust disaster preparedness.

Connectivity in a Globalized World

While physical location is crucial, digital connectivity is equally significant in 2025. Buyers prioritize areas with high-speed internet infrastructure, especially in remote and semi-urban locations. Additionally, proximity to major transportation hubs like airports and high-speed rail stations remains a top consideration for frequent travelers and global citizens.

Cultural and Lifestyle Appeal

Lifestyle trends continue to shape location preferences. Areas with thriving cultural scenes, diverse dining options, and green spaces are attracting millennials and Gen Z buyers. Regions offering niche experiences—such as wine country retreats or mountain escapes—are experiencing a boom in demand as buyers seek homes that double as lifestyle upgrades.

Conclusion

In 2025, location remains the cornerstone of real estate decision-making. Whether it’s proximity to essentials, climate resilience, or digital connectivity, buyers are prioritizing locations that align with their evolving needs. As the market continues to shift, understanding the power of location will be key to making smart real estate investments.

If you’re considering buying or investing in real estate, remember: you can change a home’s design, but you can’t change its location. Choose wisely, and your investment will stand the test of time.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Lamas Loans, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Understanding the Rate Float Down: A Comprehensive Guide

In the ever-evolving world of mortgage loans, understanding the various options available to borrowers is crucial. One such option that has gained popularity in recent years is the Rate Float Down. As we navigate through 2025, it’s essential to grasp the concept of a Rate Float Down and how it can benefit potential homeowners in Florida and beyond.

What is a Rate Float Down?

A Rate Float Down is a mortgage feature that allows borrowers to lock in an interest rate while still having the flexibility to take advantage of lower rates if they decrease before closing. This option is particularly appealing in a fluctuating interest rate environment, as it provides a safety net for borrowers who want to secure a favorable rate without missing out on potential savings.

For instance, if a seller lists their home at $300,000, a buyer may offer $290,000, and after some negotiation, they might settle on a sales price of $295,000. This agreed-upon price becomes the basis for the purchase contract, which legally binds both parties to the transaction.

However, it’s important to note that the sales price is not the ultimate determinant of the home’s value. Just because you’re willing to pay $295,000 doesn’t mean the property is objectively worth that amount. That’s where the appraised value comes in.

How Does a Rate Float Down Work?

When a borrower opts for a Rate Float Down, they initially lock in an interest rate with their lender. This locked rate serves as a ceiling, ensuring that the borrower won’t have to pay a higher rate if market rates increase. However, if interest rates drop before the loan closes, the borrower has the opportunity to “float down” to the lower rate, potentially saving thousands of dollars over the life of the loan.

It’s important to note that not all lenders offer Rate Float Down options, and those that do may have specific terms and conditions. Typically, there is a fee associated with this feature, which can vary depending on the lender and the specifics of the loan.

Benefits of a Rate Float Down

Protection Against Rising Rates: The primary advantage of a Rate Float Down is the protection it offers against rising interest rates. By locking in a rate, borrowers can rest assured that they won’t be subject to higher rates if the market shifts unfavorably.

Potential Savings: If interest rates decrease after the initial rate lock, borrowers can take advantage of the lower rates, resulting in significant savings over the life of the loan. This flexibility can be particularly beneficial in a volatile market.

Peace of Mind: The Rate Float Down option provides peace of mind to borrowers who may be concerned about the unpredictability of interest rates. Knowing that they have the opportunity to secure a lower rate if it becomes available can alleviate stress and uncertainty.

Considerations and Limitations

While the Rate Float Down option offers several benefits, there are also some considerations and limitations to keep in mind:

Fees: As mentioned earlier, there is usually a fee associated with the Rate Float Down feature. Borrowers should carefully evaluate whether the potential savings outweigh the cost of the fee.

Availability: Not all lenders offer Rate Float Down options, and the terms and conditions can vary significantly. It’s essential to shop around and compare different lenders to find the best option for your specific needs.

Timing: The timing of the rate lock and the float down can impact the overall savings. Borrowers should work closely with their lender to determine the optimal time to lock in a rate and monitor market trends to make informed decisions.

Rate Float Down in 2025: What to Expect

As we move through 2025, the mortgage market continues to be influenced by various economic factors, including Federal Reserve policies, inflation rates, and global economic conditions. In January 2025, the Federal Reserve opted to hold interest rates steady, ending a succession of three consecutive rate cuts in late 2024. However, financial markets are currently pricing in at least two rate cuts by the end of this year.

Given this context, the Rate Float Down option remains a valuable tool for borrowers looking to navigate the uncertainties of the mortgage market. With the potential for interest rates to fluctuate throughout the year, having the flexibility to lock in a rate while still being able to take advantage of lower rates can provide significant financial benefits.

Conclusion

In conclusion, the Rate Float Down is a powerful mortgage feature that offers borrowers the best of both worlds: protection against rising interest rates and the potential for savings if rates decrease. As we navigate the complexities of the mortgage market in 2025, understanding and utilizing options like the Rate Float Down can help borrowers make informed decisions and secure favorable loan terms.

Whether you’re a first-time homebuyer or looking to refinance your existing mortgage, exploring the Rate Float Down option with your lender can provide peace of mind and financial security in an ever-changing market.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Lamas Loans, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

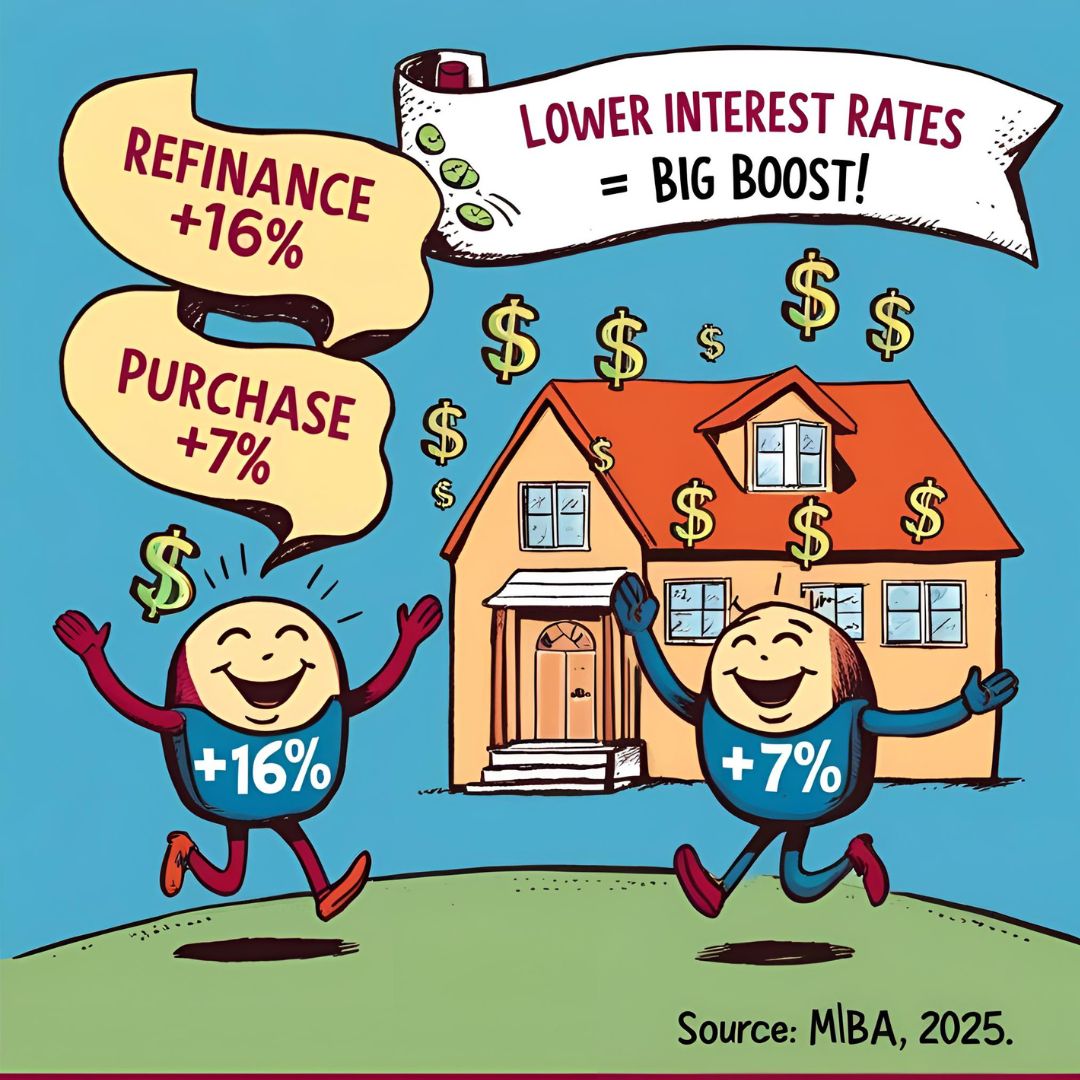

How Lower Interest Rates Boosted Refinances by 16% and Purchases by 7%, According to MBA

Mortgage applications have surged by 11.2% as interest rates continue to decline, marking a significant shift in the housing market. According to the Mortgage Bankers Association (MBA), refinance applications jumped by 16%, while purchase applications rose by 7%. This trend is a clear indicator of renewed activity in the mortgage sector, offering both challenges and opportunities for borrowers, lenders, and real estate professionals. Below, we’ll explore the reasons behind this increase, its importance for mortgage loans, and how to capitalize on the current market dynamics.

Why Mortgage Applications Are Rising

The recent rise in mortgage applications can be attributed to several key factors:

Declining Interest Rates: Mortgage rates have fallen for the sixth consecutive week, with the average 30-year fixed rate dropping to 6.67%, the lowest since October 2024. This decline has made borrowing more affordable, encouraging both new buyers and those looking to refinance.

Economic Stability: Improved economic conditions and a stable job market have boosted consumer confidence, leading to increased activity in the housing market.

Seasonal Trends: The spring homebuying season typically sees a surge in activity, and 2025 is no exception. The purchase index is now 4% higher than it was a year ago.

Government-Backed Loans: FHA and VA loans have seen significant growth, with government purchase applications increasing by 11%. Lower FHA rates, now at 6.34%, have made these loans more accessible.

The Importance of This Trend for Mortgage Loans

The rise in mortgage applications has several implications for the mortgage industry:

Increased Loan Volume: Lenders are experiencing higher demand, which can lead to increased revenue. The refinance share of mortgage activity has risen to 45.6%, up from 43.8% the previous week.

Opportunities for Borrowers: Lower rates provide an excellent opportunity for borrowers to lock in favorable terms. The average loan size for purchase applications has reached $460,800, the highest in the survey’s history.

Market Momentum: The uptick in applications signals a robust housing market, which is beneficial for the broader economy. Real estate transactions contribute significantly to local and national economic activity.

Why Now Is the Time to Refinance, Lend, and Sell: Seize the Market Momentum

For borrowers, lenders, and real estate professionals, the current market conditions offer unique opportunities:

For Borrowers:

Refinance Now: With refinance applications up by 16%, now is an ideal time to lower your monthly payments or shorten your loan term.

Explore Government-Backed Loans: FHA and VA loans offer competitive rates and lower down payment requirements, making them an attractive option.

Act Quickly: As rates may not stay low indefinitely, it’s crucial to act promptly to secure favorable terms.

For Lenders:

Streamline Processes: With increased demand, optimizing loan processing times can enhance customer satisfaction and operational efficiency.

Target Marketing: Focus on promoting refinance options and government-backed loans to attract a broader customer base.

Challenges and Considerations

While the current market presents numerous opportunities, it’s essential to be mindful of potential challenges:

Inventory Shortages: Limited housing inventory can make it difficult for buyers to find suitable properties.

Rate Volatility: Although rates are currently low, they can fluctuate based on economic conditions and Federal Reserve policies.

Affordability Issues: Rising home prices may offset the benefits of lower rates for some buyers.

Conclusion

The 11.2% rise in mortgage applications, driven by falling rates and increased refinance and purchase activity, is a significant development in the housing market. For borrowers, it’s an opportunity to secure favorable terms and achieve homeownership or financial savings. For lenders and real estate professionals, it’s a chance to capitalize on increased demand and drive business growth. By understanding the factors behind this trend and taking proactive steps, all stakeholders can benefit from the current market dynamics.

Want personalized assistance? Visit our 'Contact Us' tab and leave your information with one of our experts.

About Us

A group of like-minded seasoned veterans came together to create a company with an employee-focused culture. A culture that values its members both personally and professionally and a company built on the idea that the customer comes first!

We do not share data with third parties for marketing/promotional purposes.

By submitting your phone number to Lamas Loans, you are authorizing a representative of our company to send you text messages and notifications. Message frequency may vary. Message/data rates apply. Reply STOP to unsubscribe to a message sent from us, and HELP to receive help.

Why Mortgage Demand Surged 20% Higher and Why Now is the Best Time to Refinance

The mortgage market has been buzzing with activity recently, and for good reason. A significant drop in interest rates to their lowest levels since 2024 has sparked a surge in mortgage demand, with applications jumping by 20% in just one week. This article explores the reasons behind this surge, the implications for homeowners and buyers, and why now might be the perfect time to consider refinancing your mortgage.

The Interest Rate Drop: A Game-Changer

Interest rates play a pivotal role in the housing market. When rates drop, borrowing becomes more affordable, making it easier for people to buy homes or refinance existing mortgages. Recently, the average contract interest rate for 30-year fixed-rate mortgages fell to 6.73%, down from 6.88%. This decline, the largest weekly drop since late 2024, has been attributed to a mix of economic factors, including consumer sentiment and market uncertainties.

Lower interest rates reduce monthly mortgage payments, making homeownership more accessible. For instance, a 0.15% drop in rates can save homeowners hundreds of dollars annually, depending on the loan amount. This financial relief has encouraged both first-time buyers and seasoned homeowners to take action.

Why Mortgage Demand is Surging

The recent rate drop has had a ripple effect across the mortgage market:

Refinancing Boom: Applications to refinance home loans skyrocketed by 37% in one week and are 83% higher than the same period last year. Homeowners with higher-rate mortgages see this as an opportunity to lock in lower rates, reducing their monthly payments and overall interest costs.

Increased Purchase Activity: Mortgage applications for home purchases rose by 9% in the same week. While this is a positive sign, it’s worth noting that purchase activity remains historically low due to high home prices and limited inventory.

Seasonal Trends: The spring homebuying season typically sees increased activity, and the recent rate drop has amplified this trend.

Why Now is the Best Time to Refinance

Refinancing your mortgage can be a smart financial move, especially in a low-rate environment. Here are some compelling reasons to consider refinancing now:

Lower Monthly Payments: Refinancing to a lower interest rate can significantly reduce your monthly mortgage payments, freeing up cash for other expenses or savings.

Shorter Loan Term: If you’re financially stable, you might consider refinancing to a shorter loan term, such as 15 years. This can help you pay off your mortgage faster and save on interest over the life of the loan.

Access to Home Equity: Refinancing can also allow you to tap into your home’s equity for major expenses like home improvements, education, or debt consolidation.

Eliminate Private Mortgage Insurance (PMI): If your home’s value has increased and you now have at least 20% equity, refinancing can help you get rid of PMI, reducing your monthly costs.

Factors to Consider Before Refinancing

While refinancing offers numerous benefits, it’s essential to weigh the costs and benefits carefully:

Closing Costs: Refinancing involves closing costs, which can range from 2% to 6% of the loan amount. Calculate your break-even point to ensure the savings outweigh the costs.

Loan Term Reset: Refinancing resets your loan term, which could mean paying more interest over time if you extend the term.

Credit Score: A higher credit score can help you qualify for better rates. If your credit score has improved since you took out your original mortgage, you may benefit even more from refinancing.

The Bigger Picture

The recent surge in mortgage demand highlights the sensitivity of the housing market to interest rate changes. While the current environment presents opportunities, it’s also a reminder of the challenges many buyers face, including high home prices and limited inventory.

For homeowners, the decision to refinance should be based on individual financial goals and circumstances. Consulting with a mortgage advisor can help you navigate the options and make an informed decision.

Conclusion

The drop in interest rates has created a window of opportunity for both homebuyers and homeowners. Whether you’re looking to buy your first home, upgrade to a new one, or refinance your existing mortgage, now is the time to act. With rates at their lowest levels since 2024, the potential savings are too significant to ignore.

Take advantage of this favorable market condition, but remember to do your homework. Refinancing is not a one-size-fits-all solution, and the right choice depends on your unique financial situation. By staying informed and proactive, you can make the most of this opportunity and secure a brighter financial future.

Understanding Sales Price vs. Appraised Value and Their Impact on Your Mortgage Loan

When navigating the world of real estate, two critical concepts often come up: the sales price and the appraised value of a home. While they may seem interchangeable to first-time buyers, understanding the difference between these terms is crucial, especially when it comes to securing a mortgage loan. Let’s break down what they mean, how they differ, and how these values can influence the home-buying process.

Sales Price: The Agreed Amount Between Buyer and Seller

The sales price is the amount that a buyer agrees to pay and a seller agrees to accept for a home. This number is typically determined through negotiations between the buyer and seller, factoring in the market demand, the seller’s asking price, and the buyer’s offer.

For instance, if a seller lists their home at $300,000, a buyer may offer $290,000, and after some negotiation, they might settle on a sales price of $295,000. This agreed-upon price becomes the basis for the purchase contract, which legally binds both parties to the transaction.

However, it’s important to note that the sales price is not the ultimate determinant of the home’s value. Just because you’re willing to pay $295,000 doesn’t mean the property is objectively worth that amount. That’s where the appraised value comes in.

Appraised Value: The Objective Assessment of Worth

The appraised value of a home is determined by a licensed appraiser who evaluates the property’s worth based on a range of factors. These may include:

Comparable sales of similar properties in the area (commonly referred to as “comps”).

The size, condition, and features of the home.

Market conditions, such as supply and demand in the local real estate market.

An appraiser’s job is to provide an unbiased, professional opinion of the home’s value. For example, after inspecting the property and analyzing market data, an appraiser may conclude that the home’s value is $290,000, even though the buyer and seller agreed on a sales price of $295,000.

How Sales Price and Appraised Value Impact Mortgage Loans

The relationship between the sales price and the appraised value is critical when securing a mortgage loan because lenders rely heavily on the appraised value to determine the amount they’re willing to lend.

Here’s why: mortgage lenders aim to minimize their risk. If the appraised value is lower than the sales price, it means the buyer is agreeing to pay more for the home than its fair market value. This discrepancy raises concerns for the lender, as the property may not fully cover the loan amount if the buyer defaults and the lender needs to sell it to recoup their losses.

Scenario 1: When Appraised Value Matches Sales Price

If the appraised value aligns with the sales price, the lending process moves forward smoothly. For example, if the sales price and appraised value are both $295,000 and the buyer is approved for a mortgage, the lender will typically finance a percentage of that amount (e.g., 80% loan-to-value ratio), while the buyer covers the remainder as a down payment.

Scenario 2: When Appraised Value Exceeds Sales Price

If the appraised value is higher than the sales price, the buyer essentially gets a great deal. For instance, if the appraised value is $305,000 but the sales price is $295,000, the buyer is purchasing the home at a price below its market value. This situation rarely causes issues, as the lender is more than willing to finance a property with a higher appraised value.

Scenario 3: When Appraised Value is Lower Than Sales Price

This is where complications arise. If the appraised value is lower than the sales price, the buyer and lender must address the gap. For example, if the appraised value is $290,000 but the sales price is $295,000, the lender will typically base the loan amount on the appraised value of $290,000, not the sales price.

This means the buyer must:

Cover the difference out of pocket (in this case, $5,000).

Renegotiate the sales price with the seller to match the appraised value.

Walk away from the deal, which might be possible if a financing or appraisal contingency is included in the purchase agreement.

Why Understanding This Difference Matters

Being aware of the potential discrepancies between sales price and appraised value can save buyers from financial surprises during the mortgage process. Here are some practical tips to navigate this:

Do Your Research: Before making an offer, research comparable home sales in the area to ensure your offer aligns with market values.

Include Appraisal Contingencies: An appraisal contingency in your contract gives you the option to renegotiate or exit the deal if the appraised value comes in lower than expected.

Be Prepared for Additional Costs: In hot housing markets, bidding wars can push sales prices above appraised values. Be prepared to cover any gaps if needed.

Conclusion

Understanding the interplay between sales price and appraised value is essential for anyone entering the housing market. While the sales price reflects the amount you agree to pay, the appraised value determines the home’s objective worth and heavily influences your mortgage loan. By keeping these factors in mind, buyers can make more informed decisions, avoid unexpected costs, and set themselves up for a smoother home-buying journey.

Navigating the complexities of real estate can feel daunting, but with the right knowledge, you’ll be better equipped to handle these challenges and achieve your dream of homeownership. Let’s make smart moves together!